I was chatting with a friend of mine recently — she’s a fellow business owner — and she mentioned that her accountant doesn’t offer a pre–end of year accounts review. The result? They’d already passed their financial year-end and discovered a few nasty surprises. In addition, a number of opportunities to make smart tax efficiency and investment decisions had been missed. It’s too late to do anything about them.

It reminded me how important our own approach is here at Palmers. We always conduct a pre-end of year accounts financial review with every single client. It’s not an add-on. It’s not something we do “if there’s time”. It’s a core part of how we help clients grow their businesses — and avoid the unnecessary tax payments and stress that come with unexpected surprises.

In this guide, we’ll look into the crucial benefits of a pre-end of year accounts review and outline the key steps you can take – the same proactive steps we guide all our clients through.

First, let’s just recap on the process and purpose of the End-Of-Year Accounts.

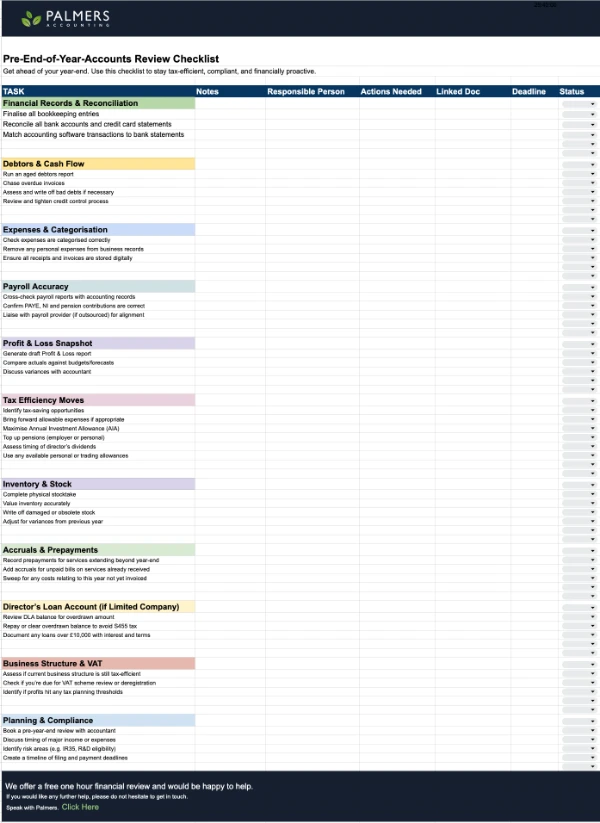

FREE PRE-END OF YEAR CHECKLIST

Use our checklist to effectively assess any areas where you could safeguad yourself or unlock extra tax savings!

Why a Pre-End Of Year Accounts Review Matters

What is a Financial Year? A financial year (also called an accounting year) is a 12-month period that a business uses to report its income, expenses, profits, and taxes. It’s the time frame covered in your annual accounts and tax returns.

Two Main Types:

- Company Financial Year (Accounting Period):

- Set when the business is incorporated (can be any start date).

- Most companies stick to this original year unless they choose to change it.

- Ends on the company’s accounting reference date (ARD).

- Common year-end accounts dates: 31 March, 30 June, 30 September, or 31 December.

- Tax Year (Personal / Sole Traders):

- Runs from 6 April to 5 April each year.

- Used for self-assessment tax returns for sole traders, partnerships, and individuals.

What Happens at Year-End?

At the end of your financial year, you are required to report the details of your business finances. You will need to:

- Finalise your bookkeeping

- Prepare annual accounts (statutory accounts preparation)

- Submit corporation tax return (if limited company year end)

- Pay any tax owed

- Review director’s loans, dividends, and retained profit

- Ensure compliance with HMRC and Companies House regulations.

Why a Pre-End Of Year Accounts Review Is Smart

Your year-end might be the official cut-off for reporting, but if you’re only looking at the numbers after that date, you can only react to discrepancies or errors, and crucially, you will have already missed valuable opportunities. Once the financial year has closed, many tax-saving or strategic moves are no longer viable..

It’s becoming increasingly standard practice — especially among proactive accounting firms like Palmers — to carry out a pre-end of year accounts review. This typically takes place 1–3 months before the year-end accounts due date, ensuring there’s still time to take advantage of tax efficiency strategies and address any issues that are highlighted.

With a timely pre-end of year accounts review, you can:

- Get clarity on your projected profit and tax bill

- Take advantage of tax allowances before they expire

- Avoid unexpected liabilities

- Strategically manage time investments, expenses, or dividends

- Tidy up any compliance issues early

In short, you go into your year-end prepared, not panicked; proactive, not reactive. It’s a crucial business financial health check.

7 Key Steps to Take Before Your End Of Year Accounts

Here are 8 fundamental steps to consider as your accounting year-end approaches. While not an exhaustive list, these cover the most critical areas for review. Want a downloadable version to keep or share with your team? Scroll down to grab your free year-end planning checklist.

1. Review Your Financial Records for Accurate End-Of-Year-Accounts

Accurate, up-to-date financial records aren’t just for compliance; they are the absolute foundation of intelligent tax planning, informed decision-making, and robust business financial health. Without a clear picture of your past transactions, it’s impossible to plan effectively for the future or ensure you’re paying the correct amount of tax for your end-of-year accounts.

Reconcile Your Bank Accounts and Credit Card Statements

- Why it matters: Unreconciled accounts are a primary source of errors in your financial reports. These inaccuracies can lead to incorrect tax submissions, misleading insights into your cash flow, and potential compliance issues down the line. It’s about ensuring every penny in your records matches reality for your year- end accounts.

- Action: Systematically match every transaction in your accounting software (e.g., Xero, QuickBooks) to your official bank and credit card statements. Identify and promptly investigate any discrepancies, regardless of their size. This includes missing transactions, duplicate entries, or incorrect amounts.

- Tip: Implement a regular reconciliation schedule – ideally weekly or monthly, rather than waiting until the end-of-year accounts deadline. This proactive approach helps catch errors early, makes the year-end process far less daunting, and provides continuous, reliable insights into your cash position. We offer bookkeeping services to keep you on top of your accounts!

Chase Any Unpaid Invoices and Assess Aged Debtors

- Why it matters: Outstanding sales invoices directly impact your business’s cash flow, severely hindering your ability to pay your own bills, invest in growth, or even cover operational costs. Uncollectible debts can also overstate your profitability and lead to paying tax on income you haven’t actually received for your year-end accounts.

- Action: Run a detailed “aged debtors report” from your accounting software. Prioritise following up on any invoices that are over 30 days past due. For significantly old or unlikely-to-be-paid debts, review whether they should be written off as “bad debt” before end-of-year accounts. Also, use this opportunity to tighten your credit control processes for the future.

- Tip: Don’t just chase; strategise. Consider offering small early payment incentives for key customers with historically slower payment habits. For persistent late payers, review your credit terms, or consider charging interest on overdue invoices if your terms allow. Read our tips on improving payments to your business and improving net cash flow.

Review Your Expense Categories – Are Items Recorded Accurately?

- Why it matters: Misclassified expenses can lead to an inaccurate understanding of your business’s true costs, distort your profit and loss figures, and potentially cause you to miss out on legitimate tax deductions. Properly categorising expenses ensures you leverage every allowable relief and provides accurate data for future budgeting and tax efficiency.

- Action: Go through your detailed expense ledger line by line. Verify that each item is assigned to the correct category (e.g., marketing, travel, professional fees, office supplies). Be cautious of personal expenses accidentally mixed with business ones, or large payments that need further breakdown.

- Tip: Maintain clear, digital records (such as receipts or invoices) for all expenses. Use features in your cloud accounting software that allow you to attach receipts to transactions. This not only streamlines your year-end accounts review but also provides irrefutable evidence for HMRC should you ever be queried.

Ensure Payroll Records Are Complete and Match Your Accounts

- Why it matters: Accurate payroll records are critical for compliance with HMRC regulations, avoiding penalties, and ensuring your employees are paid correctly. Any discrepancies can lead to significant issues with tax, National Insurance contributions, and even employment law, potentially impacting your end-of-year accounts submission.

- Action: Cross-reference your detailed payroll reports (summaries of salaries, PAYE, National Insurance, pension contributions) with the corresponding entries in your general ledger. Confirm that all payments made match the amounts recorded for wages, tax, and pension liabilities.

- Tip: If you use a separate payroll provider, ensure seamless communication and data transfer between their system and your main accounting software. Perform quarterly checks, not just annual ones, to catch and rectify any inconsistencies long before small business year-end stress sets in. We offer frequent assessment with our Payroll Services.

2. Assess Profit and Loss Position for Strategic End Of Year Accounts Decisions

Why it matters: Understanding your net profit and loss position before end of year accounts allows for proactive tax planning. Knowing your current financial performance enables you to make timely decisions that can significantly impact your tax bill and overall financial health.

Run a Draft Profit & Loss Report

- Why it matters: A draft P&L report provides a snapshot of your current financial performance, highlighting your revenues, costs, and current profit level. This insight is essential for effective year-end tax planning.

- Action: Generate a preliminary Profit & Loss report from your accounting software.

- Tip: Familiarise yourself with what a strong profit and loss statement looks like for your industry.

Compare Actuals Against Budgets/Forecasts

- Why it matters: Comparing your actual performance against your financial forecasts helps identify deviations early. This allows you to understand if you are over or under target, informing crucial decisions for your end-of-year accounts.

- Action: Lay your draft P&L against your projected budget or financial forecast for the year. Note any significant variances.

- Tip: If you don’t currently use budgeting or forecasting, now is an ideal time to start.

If Profits Are Higher Than Expected, Consider Tax-Efficient Reductions

- Why it matters: When profits are looking strong, it presents a golden opportunity for tax efficiency. By proactively investing or making certain expenditures, you can legitimately reduce your taxable profit before the year-end accounts are finalised.

- Action: Work with your accountant to identify areas where strategic investment or expenditure can reduce your tax liability.

- Tip: This is where proactive tax advice truly pays off, allowing you to turn potential tax into productive business growth.

Plan for Maximum Tax Efficiency in Your End Of Year Accounts

Why it matters: There are often tax reliefs or allowances you can only use before the financial year-end accounts. Missing these deadlines means missing out on legitimate opportunities to reduce your tax bill and improve your cash flow. Proactive planning ensures you capitalise on every available saving.

Consider Bringing Forward Allowable Expenses

- Why it matters: Accelerating certain business expenses into the current financial year can reduce your taxable profit, leading to lower corporation tax (for limited companies) or income tax (for sole traders) in your end of year accounts.

- Action: Review upcoming necessary expenditures for the next accounting period (e.g., office supplies, software subscriptions, small equipment, staff training). If appropriate and within your cash flow capacity, consider purchasing these before year-end.

- Tip: This strategy is most effective for expenses you would incur anyway. Don’t spend just for the sake of spending, but plan genuinely needed purchases strategically for tax efficiency.

Claim the Annual Investment Allowance (AIA) on Capital Purchases

- Why it matters: The Annual Investment Allowance (AIA) is a highly valuable UK tax relief that allows businesses to deduct the full value of qualifying capital expenditure from their taxable profits in the year-end accounts period of purchase, up to a generous annual limit (currently £1 million). This provides immediate and significant tax relief, encouraging businesses to invest in new equipment and machinery. Missing this opportunity means paying more tax than necessary and delaying the benefit of your investments.

- Action: Identify any planned or potential purchases of “plant and machinery” (e.g., computers, office furniture, tools, manufacturing equipment, commercial vehicles, excluding cars). If possible, make these purchases and bring them into use before your financial year-end to maximise your AIA claim for the current period.

- Tip: The AIA limit applies per-accounting-period. If your business is part of a group of companies or has multiple trades, specific rules apply. Always consult with your Palmers Accounting advisor to ensure your purchases qualify and you’re making the most effective use of the AIA. [Link to future dedicated AIA blog post & Tax Planning service page]

Top Up Pension Contributions (Personal or Employer)

- Why it matters: Both personal and employer pension contributions are highly tax- efficient. Increasing contributions before your end-of-year accounts can significantly reduce your or your company’s taxable income, offering a dual benefit of tax savings and future financial security.

- Action: Review your current pension contribution levels. If you have any available allowance, consider topping up contributions before year-end.

- Tip: Employer contributions can be offset against company profits, while personal contributions extend your personal tax savings. This is a key area for proactive tax advice.

Evaluate Whether a Director’s Dividend Makes Sense Now

- Why it matters: For limited company year end, strategically timed directors’ dividends can be a highly tax-efficient way to extract profits from your company, especially when considering your personal tax situation.

- Action: Work with your accountant to review your company’s available distributable reserves and your personal tax position to determine if declaring a dividend before year-end is the most tax-efficient method of remuneration.

- Tip: Dividends are taxed differently from salaries. A balanced approach often yields the best overall tax efficiency for a limited company’s year-end.

Use Up Tax-Free Allowances

- Why it matters: Various tax-free allowances exist (e.g., the £1,000 trading allowance or property allowance). Ensuring you’ve utilised these can contribute to your overall tax efficiency, especially for small businesses’ year-end or individuals with mixed income sources. This also includes making use of pension contributions — tax relief on pensions can help reduce your taxable income if you act before the end of the tax year.

- Action: Familiarise yourself with any personal tax-free allowances that may apply to your circumstances and ensure they are fully utilised if applicable.

Tip: Your accountant can help identify all relevant allowances and ensure they are correctly applied in your year-end accounts submissions.

3. Take Stock – Literally – For Accurate End-Of-Year Accounts

Accurate stock valuation directly affects your cost of sales, which in turn impacts your reported profit and loss figure and, consequently, your tax bill. Over- or under-valuing stock can lead to significant discrepancies in your end of year accounts.

Count and Value Your Stock at Year End

- Why it matters: A precise physical count of your inventory is fundamental to ensuring your year-end accounts accurately reflect your business’s assets and profitability.

- Action: Perform a thorough physical stocktake of all inventory held as of your financial year-end. Ensure all items are counted and recorded.

- Tip: Schedule your stocktake carefully to minimise disruption to your operations.

Write Off Obsolete or Damaged Inventory

- Why it matters: Holding onto obsolete, damaged, or slow-moving stock inflates your asset value and artificially boosts your reported profit, leading to higher tax liabilities. Writing it off provides a legitimate reduction in your taxable profit for end-of-year accounts.

- Action: Identify any inventory that is no longer saleable at full value, is damaged, or is highly unlikely to sell. Document these items for write-off.

- Tip: Maintain clear documentation (photos, disposal records) for any stock write-offs to support your tax efficiency claims.

Adjust for Any Significant Variances from Your Previous Stock Levels

- Why it matters: Comparing your current stock levels to previous periods helps identify trends, potential theft, or inefficiencies in your inventory management. Adjusting for these variances ensures your year-end accounts are as accurate as possible.

- Action: Compare the current stocktake results with your inventory records and previous year-end accounts figures. Investigate any significant discrepancies and make necessary adjustments.

- Tip: This review can provide valuable insights into your purchasing and sales processes, improving future business financial health.

4. Check for Accruals and Prepayments for Precise Year-End Accounts

Adjusting for accruals and prepayments is crucial for adhering to the accrual basis of accounting. This ensures your end-of-year accounts accurately reflect your income and expenses in the period they were earned or incurred, not just when cash changed hands, leading to more precise tax efficiency.

Identify Any Services Paid in Advance (Prepayments)

- Why it matters: Costs like annual software subscriptions or insurance premiums often cover a period beyond your current financial year-end. Failing to apportion these correctly overstates your current year’s expenses and understates your profit, leading to an inaccurate picture for year-end accounts.

- Action: List any expenses you’ve paid for upfront that relate, in part or whole, to the next accounting period. Calculate the portion of the expense that should be carried forward as a prepayment.

- Tip: Common prepayments include rent, insurance, subscriptions, and annual service contracts.

Add Any Accrued Expenses (Unpaid Bills for Services Already Received)

- Why it matters: Accrued expenses are costs you’ve incurred within the current financial year for which you haven’t yet received an invoice or made payment. Ignoring these means your end-of-year accounts will understate your expenses and overstate your profits, affecting tax efficiency.

- Action: Review services or goods received towards the accounting year-end (e.g., utility bills for the last month, legal fees, contractor work) for which you anticipate an invoice shortly after the year-end. Record these as accrued expenses.

- Tip: Ensure you’ve captured all costs that relate to the current accounting period, even if the invoice comes later, for a truly accurate business financial health check.

Review if You’ve Captured All Costs That Relate to the Current Accounting Period

- Why it matters: This final check ensures a complete and accurate financial picture. Missing costs can result in an inflated profit figure and potentially overpaying tax for your year-end accounts.

- Action: Conduct a final sweep for any outstanding invoices or known expenses that pertain to the period leading up to your year-end.

- Tip: Maintaining a sound bookkeeping system throughout the year significantly simplifies this review.

5. Review Director’s Loan Account for Limited Company Year End Compliance

Why it matters: For a limited company year-end, an overdrawn Director’s Loan Account (DLA) can lead to significant tax penalties for the company under Section 455 of the Corporation Tax Act. Furthermore, it could result in a Benefit-in-Kind charge for the director, impacting their personal tax liability. Proper management is vital for achieving tax efficiency and compliance.

Make Sure Your Director’s Loan Account is Repaid or Cleared Appropriately

- Why it matters: Clearing an overdrawn DLA before the end of year accounts submission deadline avoids the S455 tax charge (currently 33.75% on the outstanding amount 9 months and 1 day after the year-end).

- Action: If the DLA is overdrawn, ensure the director repays the amount to the company, or that the balance is cleared by declaring a formal dividend or salary, before the relevant deadline (usually 9 months after year-end).

- Tip: Plan ahead! Regular monitoring of the DLA throughout the year can prevent a large, unexpected balance at the small business year-end.

Avoid Interest-Free Loans Over £10,000 Without Proper Documentation

- Why it matters: Loans from a company to a director exceeding £10,000 (and not repaid within the tax year) can be treated as a “Benefit in Kind” by HMRC unless commercial interest is charged. This can result in additional personal tax for the director.

- Action: Ensure any DLA balances are either below £10,000, repaid promptly, or that appropriate interest is charged and declared if the loan exceeds this threshold. Document all loan terms clearly.

- Tip: Always discuss director remuneration and loan account strategies with your Palmers accountant to ensure tax efficiency and compliance for your limited company year-end.

6. Evaluate Business Structure and Planning for Future Growth

The accounting year end is a strategic inflection point to review how your business is operating. As your business grows and profits change, the legal structure that once made sense might no longer be the most tax-efficient or best suited for your long-term goals.

Is Your Business Structure Still Tax-Efficient?

- Why it matters: The choice between being a sole trader, partnership, or limited company year-end has significant implications for your tax liabilities, administrative burden, and personal liability. An outdated structure could be costing you money.

- Action: Consider whether your current legal structure (e.g., sole trader vs. limited company) still optimally suits your current profitability, administrative capacity, and future growth plans.

- Tip: This is a crucial conversation point for your pre-end of year accounts review with your accountant, especially if you’re a small business year-end looking to scale.

Are You Due for a VAT Scheme Review or Deregistration?

- Why it matters: Your VAT scheme should evolve with your turnover and operational needs to maintain optimal tax efficiency and compliance. Missing a threshold or staying on an unsuitable scheme can lead to unnecessary costs or administrative headaches.

- Action: If your turnover is approaching the VAT threshold, or if your business model has changed, review whether your current VAT scheme (e.g., standard, cash accounting, flat rate) is still the most beneficial. Also, consider whether deregistration is appropriate if your turnover drops below the threshold.

- Tip: Don’t let VAT thresholds sneak up on you. Plan ahead with your accountant to ensure smooth transitions and continued tax efficiency.

Are Your Profits Hitting Thresholds That Could Trigger Tax Planning Needs?

- Why it matters: Certain profit levels can trigger higher tax rates, reduce access to specific allowances, or change reporting requirements. Being aware of these thresholds allows for proactive tax planning to mitigate their impact on your end of year accounts.

- Action: Discuss your projected profits with your accountant to identify any upcoming tax thresholds (e.g., corporation tax rate changes, personal income tax brackets).

- Tip: This is a key part of proactive tax advice – understanding future implications helps you make smarter decisions today.

7. Book a Year-End Review Meeting for Proactive Accounting & Planning

A proactive conversation with your proactive accounting partner before your accounting year-end is invaluable. It’s your opportunity to move beyond just compliance and unlock significant savings, identify strategic opportunities, and mitigate potential risks that impact your end-of-year accounts.

Discuss Opportunities to Defer or Accelerate Income/Expenses

- Why it matters: Strategic timing of income recognition and expense incurrence can significantly influence your taxable profit for the current financial year, contributing directly to your tax-efficiency. For example, adjusting the timing of a dividend or bonus may reduce your tax liability — the current tax bands can help you identify where thresholds change.

- Action: In your meeting, review any large upcoming invoices or major expenditures with your accountant to see if there are tax-efficient benefits to timing them differently.

- Tip: This requires a detailed understanding of your business operations and future plans, making your accountant an essential partner.

Identify Risk Areas

- Why it matters: Proactively identifying potential risk areas (e.g., IR35 compliance for contractors, eligibility for R&D claims, implications of EIS/SEIS if you’re raising funding) allows you to address them before they become costly problems for your end of year accounts.

- Action: Use your review meeting to specifically ask your accountant about any emerging compliance risks or complex areas relevant to your business.

- Tip: Stay informed about changes in tax legislation, as these can introduce new risks or opportunities for tax efficiency.

Create a Timeline for Filing Deadlines

- Why it matters: Missing filing deadlines for your statutory accounts preparation, corporation tax returns (CT600), or self-assessment can result in penalties from HMRC and Companies House. A clear timeline ensures compliance and reduces stress.

- Action: Work with your accountant to establish a clear timeline for all year-end accounts related filing and payment deadlines.

- Tip: Set reminders well in advance for each deadline. Your proactive accounting partner will typically manage these for you, but understanding the schedule is still beneficial for your small business year-end planning.

Download the Free End Of Year Accounts Checklist

To make things easy, we’ve turned all of this into a clear, printable checklist. Use it in your team meetings, send it to your bookkeeper, or just tick things off as you go. It’s free, and it’s packed with tips we use in real client reviews for your end-of-year accounts.

FREE PRE-END OF YEAR CHECKLIST

Use our checklist to effectively assess any areas where you could safeguad yourself or unlock extra tax savings!

What Happens When You Work with Us

At Palmers, we don’t wait for your books to close. We sit down with you before your year- end accounts and ask the right questions:

- How’s your business tracking against forecast?

- What’s your likely profit and tax bill?

- Can we take action to reduce it now to improve tax efficiency?

- Are there risks in your cash flow, margins, or structure?

- Are you ready for the year ahead — not just the year behind?

We also integrate with other critical areas of your finances, such as [cash flow forecasting], [year-end tax planning], and [growth strategy reviews], ensuring a holistic and aligned financial strategy. This proactive approach is what a true business financial health check is all about.

Final Thoughts: Get Ahead. Stay Ahead.

Far too many business owners only gain a complete financial picture after their accounting year end has passed, by which point it’s often too late to implement effective changes. That’s simply not how we operate at Palmers Accounting.

Proactive year-end planning isn’t just about compliance; it’s about making informed decisions that benefit your bottom line. At Palmers Accounting, we believe in planning ahead, not scrambling at the last minute.

That’s why we offer every client a pre-year-end review and it’s one of the most valuable services we provide. It gives you time to act before the year closes, helping you reduce your tax bill, improve your financial position, and avoid any nasty surprises.

Your pre-end of year accounts review is your chance to take control, reduce stress, and make smarter decisions for your small business year-end. It helps you:

- Avoid unexpected tax bills

- Improve cash flow

- Reinforce compliance

- Create space for investment and growth

Don’t wait until it’s too late to address your end of year accounts. Let’s review your numbers while there’s still time to make them better.

Book Your Pre-End Of Year Accounts Review Today

Don’t let another year-end accounts process catch you off guard. Connect with Palmers Accounting today to schedule your pre-end of year accounts review.

We’ll walk you through every opportunity to optimise your finances, plan strategically, and unlock your business’s full potential, ensuring maximum tax-efficiency and a stress-free close to your financial year.